The Kelly Criterion is a formula used to determine the optimal size of a series of bets.

The Kelly Criterion is a formula used to determine the optimal size of a series of bets.

Generally, in gambling scenarios (and some investing scenarios), the Kelly strategy will do better than any other strategy in the long run.

However, personal attitude to risk can conflict with Kelly and even Kelly supporters usually choose to bet a fixed fraction of the amount recommended by Kelly in order to reduce volatility, or to protect against calculation errors.

Kelly Criterion in detail…

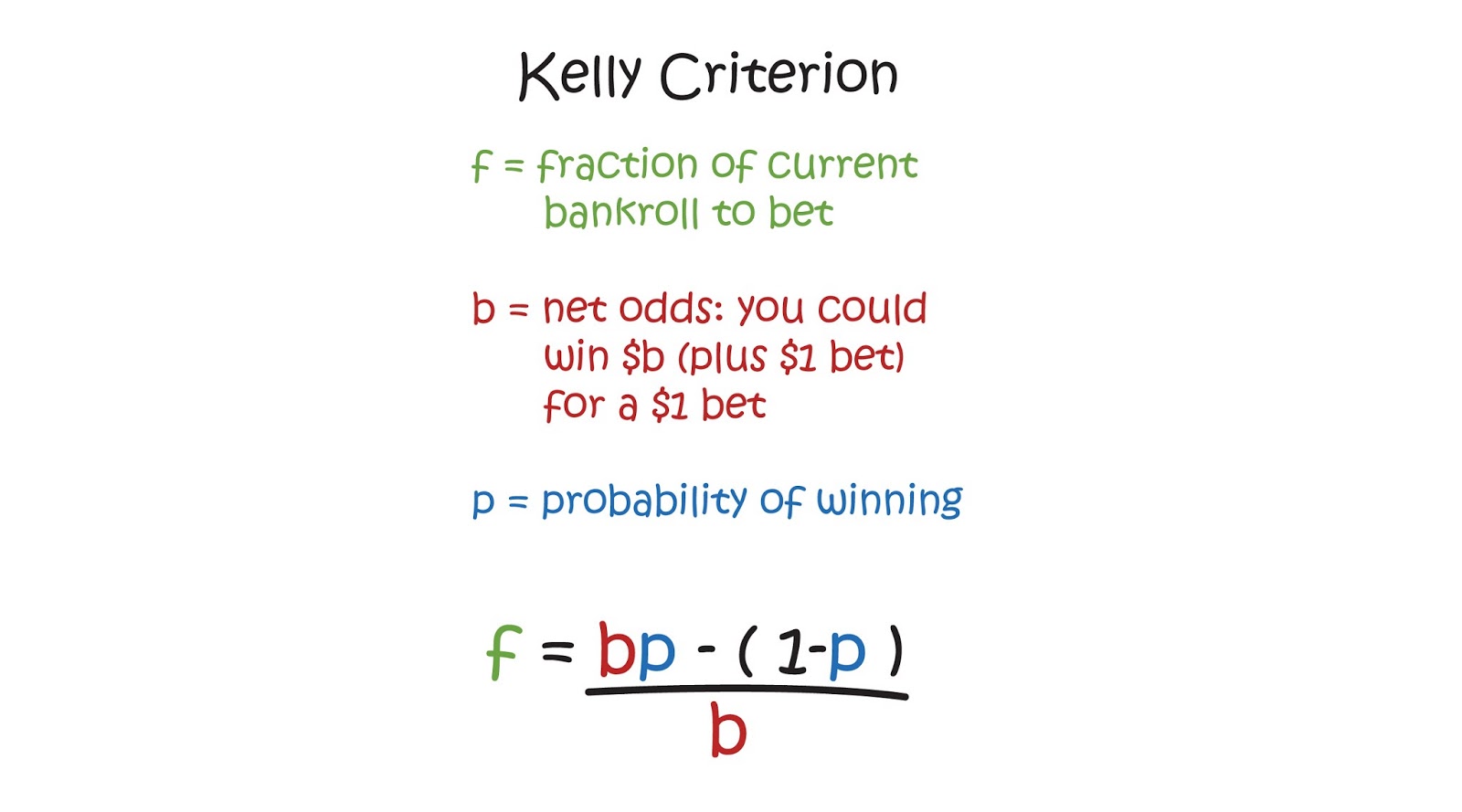

Where a bet has two outcomes (either losing the stake or winning the stake multiplied by the odds offered by the bookmaker or casino), the Kelly bet is as shown in the formula above….

Where a bet has two outcomes (either losing the stake or winning the stake multiplied by the odds offered by the bookmaker or casino), the Kelly bet is as shown in the formula above….

where f is the fraction of the bank to stake;

b is the odds for the bet (“b to 1”);

p is the probability of winning;

q is the probability of losing, which is 1 − p.

The Kelly Criterion only works where we have value in the bet.

it won’t work in a casino as the house always has the edge.

In order for f* to be positive (in other words, for you to actually have a bet) the potential payout has to be higher than one divided by the actual odds of winning.

Example 1: Black Beauty can either win a race or lose it.

Black Beauty has a price of 5/1.

You believe (after extensive form study etc…) that Black Beauty has a probability of winning of 0.2 and thus, a probability of losing of 0.8

f = (0.2 x (5 + 1) – 1) / 5 = 0.04

In other words, in this scenario we should (according to Kelly) use a stake of 4% of our bank.

Example 2: Black Beauty can either win a race or lose it.

Black Beauty has a price of 5/1.

You believe (after extensive form study etc…) that Black Beauty has a probability of winning of 0.5 and thus, a probability of losing of 0.5

f = (0.5 x (5 + 1) – 1) / 5 = 0.40

In other words, in this scenario we should (according to Kelly) use a stake of 40% of our bank.

Example 3: Black Beauty can either win a race or lose it.

Black Beauty has a price of 5/1.

You believe (after extensive form study etc…) that Black Beauty has a probability of winning of 0.1 and thus, a probability of losing of 0.9

f = (0.1 x (5 + 1) – 1) / 5 = -0.08

In other words, in this scenario we should (according to Kelly) use a stake of negative 8% of our bank.

In other words, we shouldn’t bet on Black Beauty at those odds.

But wait….

Kelly himself said that his calculations only work where you have a high number of similar “games.”

Now, no two races are identical, although system followers/users assume that they are.

Also, we can never be absolutely exact in our estimation of p (the probability of winning.)

We can study form all day long but we can never absolutely accurately predict how Black Beauty is going to perform.

He may have just had an argument with Mrs Black Beauty?

He may be worried about Baby Black Beauty’s school grades?

A car might backfire and scare him?

It is because we don’t have an infinite number of identical events and that we can never absolutely predict the possibility of winning (as we would be able to if we were rolling a dice or flipping a coin) that we bet to Fractional Kelly.

Typically we would be to half of the computed Kelly Stake but…

It can be seen that the probability of halving the bank, using full Kelly Stakes, is 50% (you have a 1/n chance of reducing your bank to 1/n of its original value.)

However, for the Half Kelly Stake, the probability of reducing the bank to half its original value is square root of what it was previously – in other words… 1/9

The downside to this sensible way of handling risk (the inevitable losing runs which will happen)is that the bank will increase more slowly, but the risks of losing it all are diminished.

Also, by using a Half Kelly Stake the volatility experienced is greatly reduced although….

So is the eventual return over any set period of time.

Betting a Half Kelly Stake, for example, reduces bank volatility by 50%, but growth by only 25%.

Conclusion

The Kelly Criterion has many critics; primarily because we cannot exactly measure the probability of winning (in horse racing, at least) and is only works where we have a large number of identical events (no two horse races are identical.)

But…

It is worth having a think about the maths behind the Kelly Criterion purely because….

It displays, quite simply, the need to have value in each and every bet.

It’s not enough just to have value (i.e. don’t back Dennis the Donkey just because you can get him at Ladbrokes at 200/1 when his real odds should be 50/1) – you can’t eat value!

You need to back the winning horse (or lay the losing one) but…

The Kelly Criterion indicates that you should stake a percentage of your bank that varies according to the confidence you have in winning the bet.

If you pop over to Top Trainers you will see that I have published four free eBooks (well, they’re free to Intelligent Betting members.)

There are another two on their way – these should be ready by the weekend and will show Jockey/Course statistics.

If you have any ideas about any reports you would like me to publish, please let me know.

Members of Intelligent Betting get the following…

Really Simple Ratings (top four rated horses)

Really Simple Ratings (all horses)

Intelligent Betting System Selections

Horse Change in Class

Horse Change in Trainer

Unique Jockey & Trainer

Raiders

System Builder (coming soon)

If you want more information about Intelligent Betting, please visit Find Out More.

As always…

My kindest regards